🚀 Introduction: A New Era for DeFi Compliance

Listen up — because this is big. The U.S. Treasury just lit a fuse under the decentralised finance (DeFi) industry, and when it blows, the landscape will never look the same again.

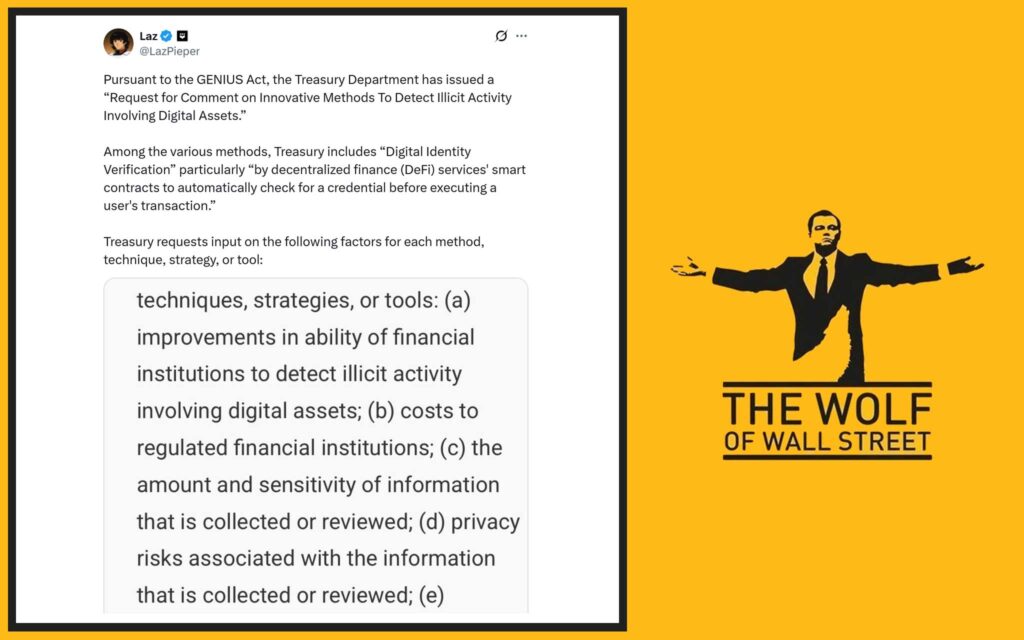

We’re talking about a government-backed push to integrate digital identity verification directly into blockchain systems. Not “optional.” Not “nice to have.” A full-on regulatory framework, courtesy of the freshly minted GENIUS Act.

And here’s the kicker: this isn’t just about chasing criminals. This is about control, compliance, and a battle that could see $6.6 trillion sucked out of U.S. banks and into the hands of stablecoin issuers. That’s trillion, with a “T.”

So, if you’re a trader, a builder, or an investor — buckle up. Because the rules of the game are being rewritten in real time.

📜 The GENIUS Act: Washington’s Big Bet on Crypto

In July 2025, the U.S. passed the GENIUS Act — legislation designed to tackle the Wild West of crypto by creating guardrails around stablecoins.

Here’s what the law demands:

- Stablecoin issuers must now fall under a regulatory framework.

- Treasury must research and implement next-gen compliance technologies.

- Public consultation is open until October 17, 2025.

Translation? Washington’s tired of watching billions flow through unregulated channels. The GENIUS Act is their way of slamming the brakes — or steering the car before it skids off a cliff.

🔍 Treasury’s Grand Consultation: Digital ID in Focus

The Treasury isn’t just throwing darts here. They’re asking the public for input on specific compliance tech — and the list reads like something out of a Silicon Valley pitch deck.

Proposed solutions include:

- Government-issued digital IDs

- Biometrics (face scans, fingerprints — you name it)

- Portable digital credentials you carry across platforms

- Blockchain monitoring with machine learning

- APIs and AI-powered tools for automated checks

This isn’t theory. These are the building blocks of a surveillance-ready DeFi system — wrapped in the promise of convenience and cost savings.

🛠️ The Tech Toolbox: Identity Meets Blockchain

Let’s cut to the chase: The government wants compliance baked into the code.

Think of it like this — right now, DeFi platforms are peer-to-peer casinos. You connect your wallet, you play, no questions asked. In the new model, your wallet itself becomes your ID card.

Your transactions won’t even process until the smart contract verifies you’ve passed KYC/AML. That’s:

- Know Your Customer (KYC) — Are you who you say you are?

- Anti-Money Laundering (AML) — Are you hiding dirty money?

And it won’t be some human behind a desk checking paperwork. It’ll be code, automated and ruthless.

🤖 Smart Contracts Meet Compliance

Here’s where it gets spicy. Imagine every smart contract on Ethereum, Solana, or any DeFi chain having compliance logic built right in.

- You want to trade? Verify.

- You want to stake? Verify.

- You want to mint a stablecoin? Verify.

If you pass — green light. If not — the blockchain slams the door in your face.

This is compliance without bankers, brokers, or bureaucrats. But it’s also compliance that never sleeps, never bends, and never forgets.

💰 Why This Matters: The Billion-Dollar Compliance Dilemma

Let’s talk money.

Traditional compliance is expensive — armies of lawyers, analysts, and auditors pouring over transactions. But Treasury’s pitch is seductive: digital identity could slash compliance costs while boosting privacy.

How? By automating everything and reducing human involvement. The promise:

- Lower costs for firms

- Fewer false positives

- Better data protection

In theory, this makes life easier for both companies and users. In practice? It centralises trust in a government-run identity system.

🛡️ The Privacy Paradox

Now here’s the paradox: DeFi was built on anonymity, freedom, and decentralisation. But digital IDs bring centralisation back to the core.

- Who controls the ID system?

- What happens if data gets hacked?

- Can governments freeze or revoke access?

Treasury says this will enhance privacy. But the crypto community knows better: privacy and control rarely mix well with regulation.

🏦 Banking Industry Panic: $6.6 Trillion at Risk

Wall Street is terrified — and for good reason.

Major U.S. banks are sounding the alarm: if stablecoin issuers can offer yield without playing by banking rules, we could see $6.6 trillion leave traditional deposits and flood into stablecoins.

That’s not just bad news for bankers. That’s catastrophic. Why? Because banks rely on deposits to fund loans. Pull the money, and suddenly credit markets dry up. Businesses struggle. Jobs vanish.

And just like that, DeFi isn’t just a quirky niche. It’s a systemic threat to the global financial order.

📊 Winners & Losers in This New Regulatory Landscape

So who comes out on top?

Winners:

- DeFi platforms that play ball and integrate compliance.

- Traders who adapt early to regulated systems.

- Innovators building compliance-as-a-service solutions.

Losers:

- Traditional banks clinging to the old model.

- Shadowy DeFi projects dodging regulation.

- Privacy maximalists who refuse digital IDs.

Make no mistake — compliance is coming. You either adapt, or you get left behind.

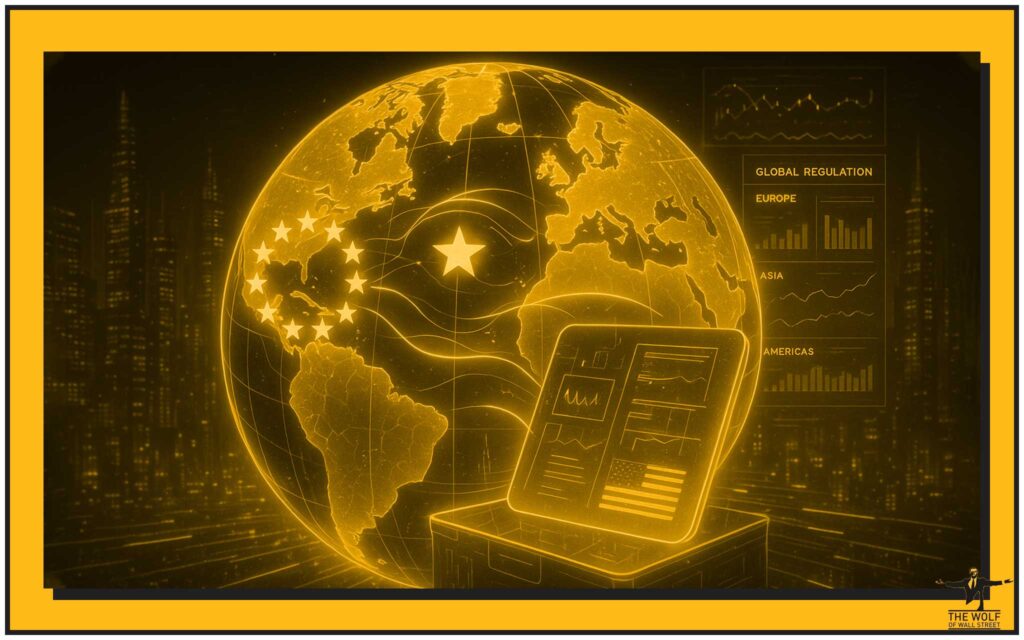

🌍 Global Perspective: Are Other Nations Ahead?

The U.S. isn’t the only player here.

- The EU is rolling out a bloc-wide digital wallet tied to its eIDAS regulation.

- Singapore and Japan are experimenting with regulatory sandboxes for compliant DeFi.

- China is already miles ahead with its state-controlled digital yuan and strict ID controls.

If America drags its feet, it risks losing ground. The GENIUS Act is Washington’s way of catching up before it’s too late.

🕵️♂️ AML & KYC: Stopping the Bad Guys Early

Let’s be clear: not all regulation is bad.

Right now, DeFi is a paradise for:

- Money launderers

- Terrorist financiers

- Sanctions dodgers

Digital ID could cut these actors off before they ever touch the system. That means more institutional money could flow into DeFi — because the risk is reduced.

🧑💻 Developers’ Dilemma: Building With Compliance in Mind

For DeFi developers, this is both a nightmare and an opportunity.

- Nightmare: extra coding, higher complexity, new liability risks.

- Opportunity: whoever cracks the compliance + UX equation will own the market.

Think about it: the next MetaMask won’t just be a wallet. It’ll be a passport to compliant DeFi.

💬 Stakeholder Reactions: Mixed Voices

- Treasury: “This is about safety and innovation.”

- Banks: “This is an existential threat.”

- Developers: “It’s possible, but it changes everything.”

- Crypto community: Split down the middle — freedom fighters vs. pragmatists.

This isn’t a technical debate anymore. It’s ideological.

⏳ The Countdown: What Happens After October 17?

The clock is ticking. After the consultation ends:

- Treasury drafts a report for Congress.

- New rules or guidance could follow.

- Implementation could begin within 12–18 months.

Translation? By 2027, DeFi as you know it today could be unrecognisable.

🚨 What You Should Do Right Now

- Traders: Start preparing for KYC-gated DeFi platforms.

- Developers: Build compliance hooks into your projects now.

- Investors: Watch policy moves like hawks. Regulation creates winners and losers — don’t be on the wrong side.

For extra firepower, tap into expert insights and real-time support inside the The Wolf Of Wall Street crypto trading community.

📈 The The Wolf Of Wall Street Edge: Master DeFi With Insider Access

Let’s cut the fluff. If you’re serious about making money in crypto — you can’t navigate this alone.

That’s where The Wolf Of Wall Street comes in:

- Exclusive VIP Signals: Maximise profits with insider-grade trading alerts.

- Expert Market Analysis: Stay ahead with insights from top-tier traders.

- Private Community: Over 100,000 members sharing strategies 24/7.

- Trading Tools: From volume calculators to pro-level dashboards.

- 24/7 Support: Real humans, real answers, whenever you need them.

👉 Start here: The Wolf Of Wall Street Service

👉 Join the conversation: The Wolf Of Wall Street Telegram

✅ Conclusion: The Future of DeFi Regulation Is Here

Here’s the bottom line:

The U.S. Treasury isn’t asking if DeFi will be regulated. They’re asking how. And digital identity is the weapon of choice.

This isn’t the end of DeFi. It’s the evolution of DeFi. For those who adapt, the upside is limitless. For those who resist, the clock is ticking.

The next generation of crypto wealth won’t be made by dodging regulation — it’ll be made by mastering it.

❓ FAQs

1. What is the GENIUS Act and why does it matter for DeFi?

It’s a law passed in July 2025 that regulates stablecoin issuers and pushes Treasury to integrate compliance tools like digital IDs into DeFi.

2. How would digital ID integration work in smart contracts?

Compliance checks (KYC/AML) would be embedded directly into the code, automatically verifying users before transactions execute.

3. What are the risks for traditional banks?

If stablecoins become yield-bearing alternatives, U.S. banks could lose up to $6.6 trillion in deposits.

4. How does this affect my crypto trading today?

Nothing immediate — but within 1–2 years, expect KYC requirements across most DeFi platforms.

5. Can DeFi remain decentralised under regulation?

Partially. The tech will remain decentralised, but access will be gated by centralised digital identity systems.